A Swiss Re study paints stable future for the insurance sector across the globe:

Global reinsurance major Swiss Re, in a recent study titled ‘Growth in the shadow of (geo)politics – Global economic and insurance market outlook 2025-26’, maintains that the primary non-life insurance industry is improving its profitability and economic sustainability, arguing that underwriting results benefited from easing inflation and higher premium rates in 2024 and this may stay strong in 2025 and 2026.

“Coupled with improving investment results, this should support profitability. We forecast industry ROE at 10% in 2025 and 2026 in the 6 largest non-life insurance markets, which would exceed cost of capital. A more resilient industry is better positioned to reduce protection gaps, particularly when the capital base is strengthened, states the study adding, however, social inflation is not slowing in the US and rising costs of legal awards are also emerging in markets such as the UK, Australia and Mexico, impacting casualty insurers.

NON-LIFE PREMIUM GROWTH

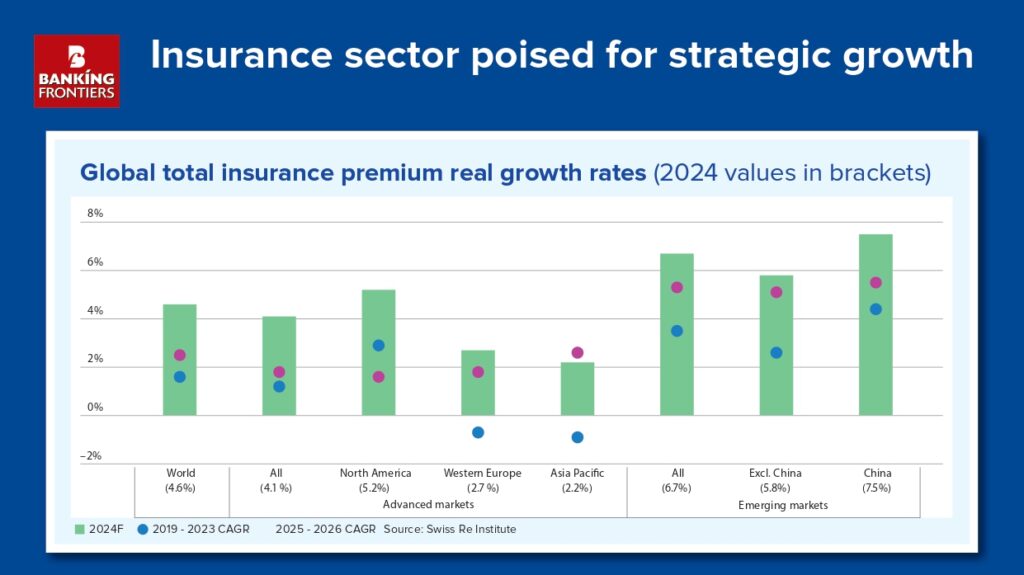

Swiss Re expects decade-high 4.3% global non-life premium growth this year following the repricing of risk in response to elevated claims. Premium rates are now moderating, it says, maintaining that softer global premium growth of 2.3% annually in real terms over 2025-26, below the 3.1% average of the last five years.

LIFE PREMIUM TOO

The study says the total global life insurance premiums should reach US$4.8 trillion by 2035, up from US$3.1 trillion in 2024, driven by higher interest rates. US individual annuity sales should reach a new record of over US$400 billion this year and as monetary policy loosens, fixed rate annuity sales growth could slow and the focus shift to indexed annuities.

PRIMARY INSURANCE

Swiss Re says the global primary insurance market will see above-trend growth in the next 2 years as the non-life hard market reaches an inflection point and life insurance sales ease from recent highs. “We forecast 2.6% total global real premium growth on average in 2025 and 2026, lower than 2024 (4.6%), but higher than the past 5 years (2019-2023 average: 1.6%). Steady global economic growth, resilient labour markets, rising real incomes as inflation moderates, and still elevated long-term interest rates will support demand. In non-life, rates on commercial lines of business are moderating while personal lines rates have further to rise. Non-life underwriting profitability will improve as lower

inflation gradually eases claims severity,” says the study.

The study says for life insurers, demand for savings products is to moderate as interest rates decline, and risk protection products will play a larger role in growth in the next 2 years.

According to the study, life and non-life (including health) premiums accounted for 43% and 57% of total premium in 2024, and this mix is likely to stay largely the same over the next decade. It is expected that in property and casualty (P&C) insurance, improving economic sustainability and profitability could be there in the next 2 years, supported by the recent re-pricing of risk. Similarly, health insurance premium growth is expected to outpace P&C segment growth in 2025 and 2026 due to rising demand for health coverage and medical cost inflation.

CAPITAL INFLOWS EXPECTED

Another major aspect is that more sustainable profitability in the re/insurance industry typically attracts capital inflows, which, by improving access to coverage, can create opportunities to reduce protection gaps. “Stronger profits, improved terms and conditions, progress on disinflation and higher investment income are all increasing the competitive pressure for downward price adjustments. The rate hardening forces that followed the inflation surge in 2021 and 2022 are fading and the outlook for pricing is now more moderate. However, trends such as social inflation and rising natural catastrophe losses have the potential to counteract market softening in related portfolios,” says the study.

The study predicts global non-life premium growth to slow as pricing conditions become less favourable, led by advanced markets. Global non-life premiums could decelerate to a 2.3% CAGR over the 2025-26 period – below the 4.3% growth rate of 2024 and the 3.1% CAGR of the last 5 years.

Price moderation will impact advanced markets the most in the next 2 years, says study, adding the US market, which accounts for 58% of global non-life premiums, is expected to slow from 4.7% real growth in 2024 to a 1.9% CAGR in 2025-26, lower than the 3.4% CAGR of the past 5 years, as competition builds. In Europe, the trend could be Germany (from 4.5% to 1.0%, vs 1.2% in 2019-23), Italy (from 6.6% to 1.8%, vs 0.2% in 2019-23) and the UK (from 3.0% to 0.8%, vs 2.3% in 2019-23).

The study also says in emerging markets, growing exposure rather than pricing is supporting premium growth. Swiss Re expects a CAGR of 4.1% during 2025-26, slightly below the 4.3% of 2024 and higher than the 3.7% average of 2019-23.

EMERGING ASIA CRUCIAL

It points out that emerging Asia is its main driving force, where non-life premiums are expected to grow at a 7.4% CAGR in 2025-26 as India outperforms all major emerging markets. “We forecast India’s non-life premium growth at 8.0% and 9.3% in 2025 and 2026 respectively, driven by strong economic growth, with rising demand for auto insurance, health coverages and government support for crop insurance,” says the study.

As regards, China, the study says there could be a 4.1% CAGR in the non-life sector in 2025-26, below the 9.8% CAGR of the past decade, as weaker consumer confidence and economic activity weigh on demand. The economic stimulus may benefit cycle-sensitive insurance lines like motor and fiscally reliant segments like agriculture. It also says health insurance could be growing faster than other lines, albeit at a slower pace than recent years, reflecting China’s ageing population, rising medical inflation and government incentives.

The study says underwriting results have strengthened from the combination of higher premium rates and easing claims growth in 2024. “We estimate a net combined ratio of 98% in 2024, an improvement from 102% in 2023. In 2025 and 2026, we estimate that P&C underwriting profits will remain positive at around the same levels as in 2024,” says the study.

CYBER INSURANCE MARKET

Describing cyber threats as a rising aggregation risk in a softening market, the study says the volume of malicious cyberattacks worldwide jumped by 75% year-on-year in 3Q24, a sign of growing sophistication of cybercriminals and more geopolitical conflict. It says: “Cyber risk is the top cause of concern for corporates for the third year in a row. Yet pricing in the cyber insurance market is softening and coverages are widening due to a moderation in attritional losses, thanks to better cyber hygiene and prudent underwriting on the part of insurers. However, the pricing outlook seems more differentiated as concerns around large systemic cyber losses intensify in the wake of Generative AI adoption and geopolitically motivated cyberattacks against critical infrastructure.”

The study says the global cyber insurance market size is expected to reach US$16.6 billion by 2025. However, sustainable growth will largely depend on managing systemic exposures from both malicious and non-malicious sources.

It says: “The CrowdStrike outage incident in July 2024 highlighted the aggregation risk from non-malicious events, where losses can quickly accumulate across software supply chains and challenge the capabilities of current cyber risk models. For the re/insurance industry and its clients, this will likely need more investment in areas such as data collection, risk modelling and contract consistency. The industry may also need additional capacity, generated from capital markets and/or government backed programmes, to close the protection gap.”

DOUBLE GROWTH FOR LIFE PREMIA

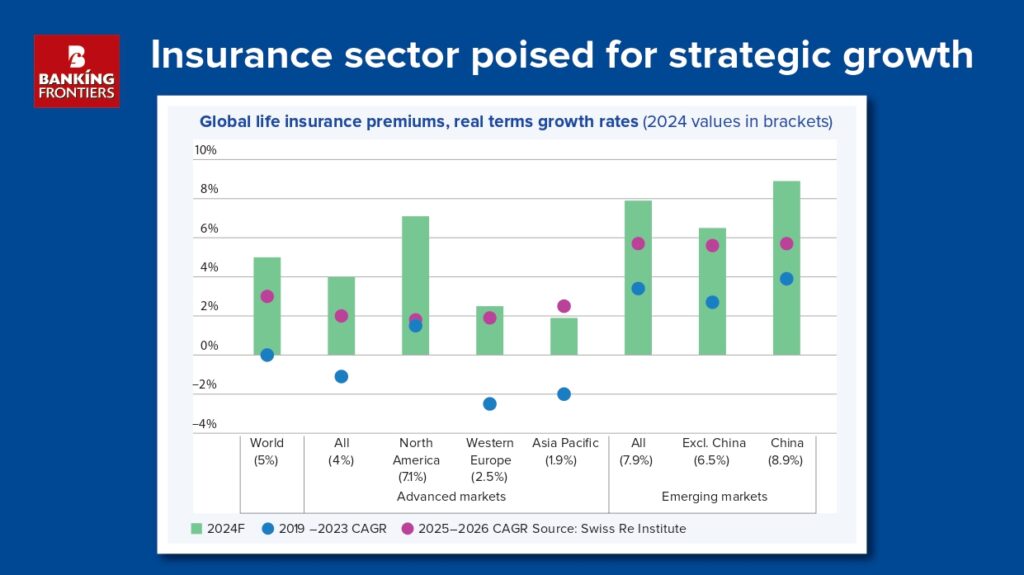

As regards life insurance, the study says global life premiums are set to grow at more than double their historical pace over 2025-26 after growing by 5% in 2024.

The global life market is expected to reach US$4.8 trillion by 2035 and life insurance global premium growth and reinvestment yields will both reach a peak in 2025 and there could be strong, above-average premium growth for the next 2 years. Also, global life premiums could grow by a CAGR of 3% in real terms in 2025-26, more than double the past long-term trend (CAGR of 1.3% during 2014-23). The global life market grew by 5% in 2024, the highest rate in a decade, primarily driven by strong demand for savings products.

The study forecasts global life insurance premiums to reach US$4.8 trillion by 2035, up from US$3.1 trillion in, bringing the life insurance market share up to 43% of global insurance premiums.

The study says advanced markets will grow by 2% annually on average in 2025-26 in real terms and growth is normalizing due to strong base effects from 2024, with North America the key driver (2025-26 CAGR: 1.8%, down from 7.1% in 2024). In emerging markets, there could be a real CAGR of 5.7% in 2025-26, also above the long-term trend (CAGR 2019-23: 3.4%), driven by China and India (2025-26 CAGR of 5.7% and 5.8%, respectively).

Recent Articles:

RegTech Trends: How Banks Are Automating Compliance Management