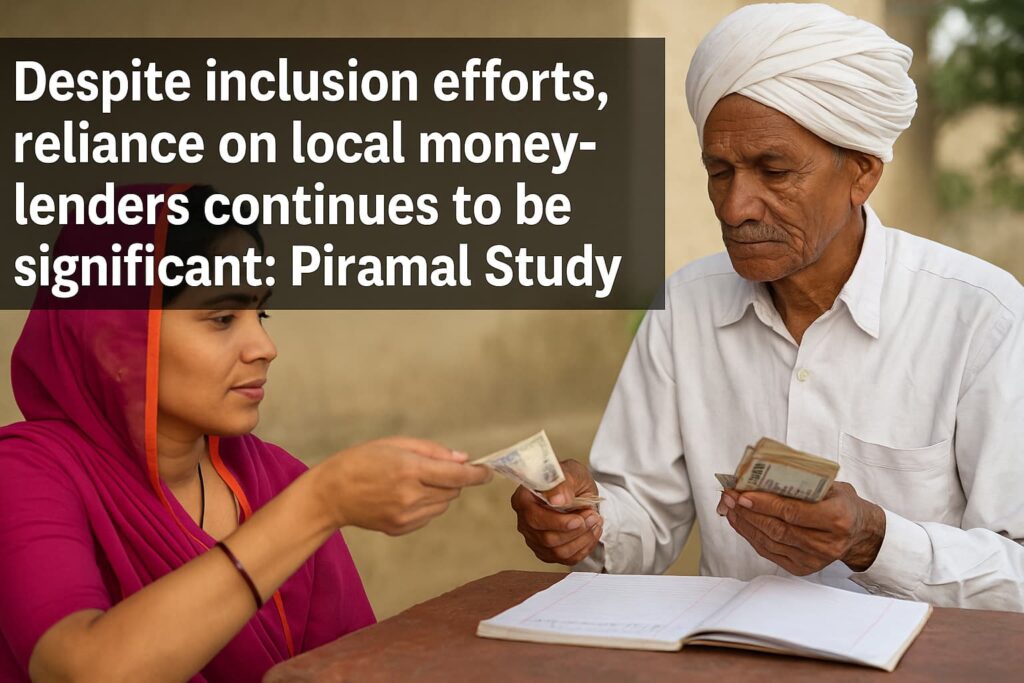

Despite significant strides in financial inclusion initiatives, such as the Pradhan Mantri Jan Dhan Yojana (PMJDY) since 2014, a new analysis by Piramal Enterprises reveals that Indian households, particularly vulnerable segments, continue to heavily rely on non-institutional channels, including local moneylenders, shopkeepers, and personal networks.

Although there were early signs of a shift from non-institutional to institutional borrowing between FY15 and FY19, the disruptions caused by COVID-19 and the accompanying rise in unemployment reversed this trend, the report states.

Many borrowers were compelled to return to informal lenders, a pattern that coincided with large-scale urban-to-rural reverse migration and a subsequent increase in agricultural employment triggered by the 2020 lockdowns. Consequently, India continues to have a low penetration of institutional credit, with a credit-to-GDP ratio of 55.63% in 2024, increasing marginally from 53.36% in 2014.

For the period between 2011 and 2021, while other economies, both developed and developing, witnessed a declining trend in the share of non-institutional credit, India observed rising incidences of non-institutional lending, vis-à-vis institutional lending. In 2021, borrowing from non-institutional sources was 2.63x of borrowing from institutional sources in India, compared to 0.6x in Brazil or 0.27x in the USA. This implies that for every two people borrowing from institutional sources, 5 people opted for non-institutional sources of borrowing.

The data used for this analysis was sourced from the Centre for Monitoring Indian Economy’s (CMIE’s) Consumer Pyramid Household Survey (CPHS) dataset.

To curb the trend of heavy reliance on informal moneylenders, especially post-COVID-19, targeted policy measures are needed to provide reliable institutional financial services to economically vulnerable groups, including EWS, LIG, blue-collar workers, and small businesses. NBFCs are at the forefront to take this responsibility, with agile underwriting processes, robust risk management and presence across the last mile of the economy, states the report.

To enhance their role, the report suggests supporting NBFCs in reducing their funding costs, which can then be passed on to borrowers. Proposed measures include:

· A liquidity backstop window from the RBI for top-tier NBFCs to improve credit ratings and reduce borrowing costs.

· Granting deposit-taking licenses to well-managed, large NBFCs, with appropriate regulatory safeguards, would allow these institutions to diversify funding sources beyond banks and raise long-term liabilities at lower costs, thereby reducing ALM.

· A dedicated refinancing window for NBFCs is urgently needed to alleviate liquidity concerns.

· Simplifying the ease of doing business for these institutions by lowering the loan amount threshold for enforcing security interests under the SARFAESI Act from ₹20 lakh to ₹1 lakh would be highly beneficial.

These reforms would equip NBFCs with greater capacity to expand their reach, serving a larger portion of India’s population who still struggle to access formal financial services, the report points out.